by George Lameh

Urban nature-based solutions (NBS), such as green roofs, are increasingly recognised as tools for climate adaptation. However, their integration into insurance mechanisms remains limited and context-dependent. Evidence suggests that the viability of linking NBS with insurance rests on a combination of several factors – e.g., urban structure, property ownership, regulatory frameworks, financing instruments, insurance practices and climatic conditions. NBS–insurance initiatives cannot simply be transposed from one context to another, but must be adapted to local technical, policy and market conditions (Lameh, 2026). Developing business models linking nature-based solutions and insurance is therefore not a matter of designing new financial products. It requires aligning technical feasibility, policy frameworks, market conditions and stakeholder incentives within specific urban contexts. Research carried out in the PIISA project, participated by CMCC researchers, leverages the Business Model Canvas (BMC) as an analytical framework to analyse how NBS could be integrated into insurance mechanisms.

Structuring NBS–insurance models through the Business Model Canvas

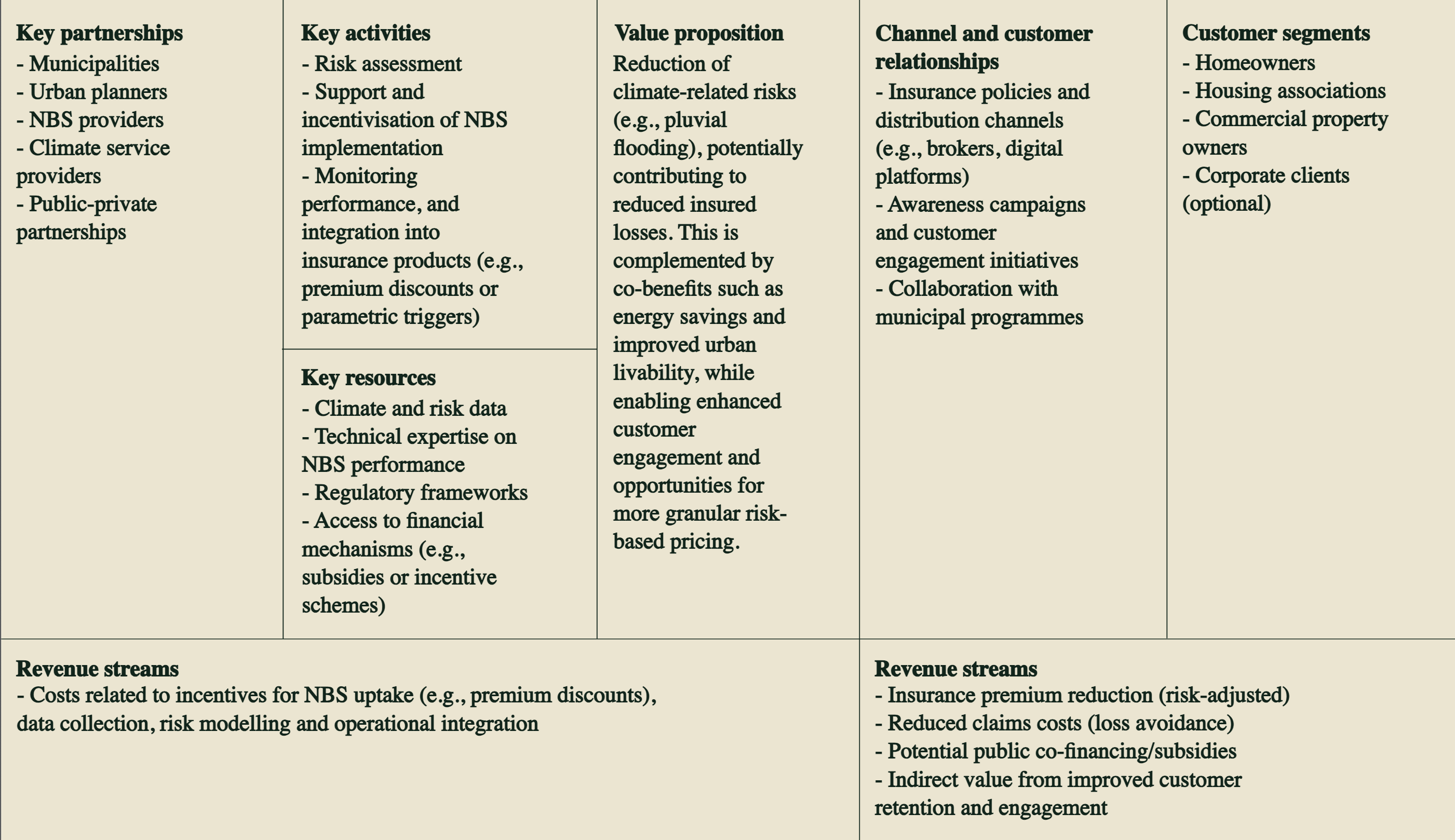

Applying the Business Model Canvas (BMC) framework to NBS–insurance interactions helps clarify how insurers could incorporate nature-based risk reduction measures into their products and services. The BMC is a widely used strategic tool that helps describe how an organisation creates, delivers and captures value. It structures a business model through its key components – value proposition, customer segments, key activities, partnerships, resources, channels, costs and revenue streams.

The table below illustrates a conceptual Business Model Canvas for the integration by insurance companies of green roofs and urban flood risk management.

Current evidence suggests that several elements central to NBS-insurance business models remain underdeveloped, particularly the quantification of risk-reduction benefits and the identification of clear revenue mechanisms.

As a result, the canvas should be interpreted primarily as a structured representation of emerging interactions between insurers, urban stakeholders and NBS providers. Moreover, alternative configurations may apply depending on the actor considered.

In addition, while the canvas discussed here adopts an insurer-centric perspective, municipalities, building owners or NBS providers could develop different business model configurations with distinct value propositions and revenue logics. Aligning the incentives and value propositions of these actors remains a central challenge for the development of viable business models.

Lessons for NBS–insurance integration

Experiences from research on green roof incentives across three contexts (the Netherlands, Nordic countries, and Italy), conducted by the PIISA project, provide a valuable testbed for the application of the BMC and the integration of NBS into insurance practices.

For instance, in Nordic countries, technical feasibility is affected by climatic constraints, while market interest remains uncertain. Whereas in Mediterranean contexts water scarcity and different urban conformation may reduce the relevance of green roofs as an adaptation measure.As a result, transferring business models between cities and contexts often proves difficult.

The Dutch context offers particularly favourable enabling conditions. Municipal subsidy schemes help reduce upfront costs for building owners, while several insurers have explored linking prevention measures to insurance incentives. In the dense urban environments exposed to pluvial flooding typically found in the Netherlands, green roofs can contribute to stormwater retention, creating a plausible value proposition for insurers interested in prevention-oriented strategies.

Even under these favourable conditions, however, developing viable business models remains challenging. The quantification of loss reduction afforded by green roofs and the cost–benefit balance for insurers is still uncertain, especially where adoption depends heavily on public subsidies or policy support.

Finally, investments in green roofs are rarely driven by climate risk reduction alone. Urban greening is often motivated by additional goals such as biodiversity gains, aesthetic improvements and efforts to improve urban liveability. While these factors can strengthen the economic rationale for rooftop greening, they do not directly benefit insurers. And they could undermine the development of a viable business case if they encourage the adoption of NBS that diminish overall risk-reduction potential.

Overall, current experience suggests that business models enabling insurers to integrate NBS into their practices remain at an early stage of development. While promising examples exist, replication potential appears moderate and often relies more on knowledge transfer, awareness-raising and supportive policies than on immediate large-scale market deployment.

Implications for replication and insurance innovation

Business models for NBS are not easily transferable between contexts. Their viability depends on local urban structures, policy frameworks, climatic conditions and market dynamics. This implies that replication rarely consists of transferring a ready-made model. Instead, successful approaches require adapting technical design, aligning with local regulations and building partnerships with relevant urban stakeholders.

While insurance can play an enabling role in supporting the adoption of NBS, it is unlikely to act as the primary driver on its own. In fact, although insurers may incorporate incentives for risk prevention into their products and services, such as premium discounts or risk assessment tools, these mechanisms often rest on supportive public policies, regulatory frameworks as well as the production of reliable evidence on the risk-reduction performance of NBS. Without such enabling conditions, insurers have limited incentives to integrate NBS-related measures into their products and services.

Lastly, the potential for replication varies significantly across sectors and hazards. In some domains, such as drought risk management in agriculture or wildfire risk management in forestry, insurance-linked services may offer clearer pathways for replication. This stems from a clearer link between preventive measures and realized risk reduction, as well as the fact that these relationships are easier to model in such contexts. In contrast, as urban NBS applications such as green roofs often rely on external strategies, progress occurs more gradually, through a combination of policy integration, stakeholder engagement and knowledge transfer. Rapid diffusion sustained by market expansion is less viable in this context.

Take home messages

Experience from green roof initiatives suggests that integrating NBS into insurance practices is still an emerging field. Its future development and success will depend on the effective alignment of technical feasibility, policy frameworks, market conditions and stakeholder capacities. Tools such as the Business Model Canvas can help structure these interactions, but their application must remain flexible and responsive to local conditions. Science, policy and practice should continue to explore avenues to facilitate this integration and interactions, as it would pave a way for insurance to evolve from a purely compensatory mechanism into a proactive tool supporting urban climate adaptation and resilience.